.svg)

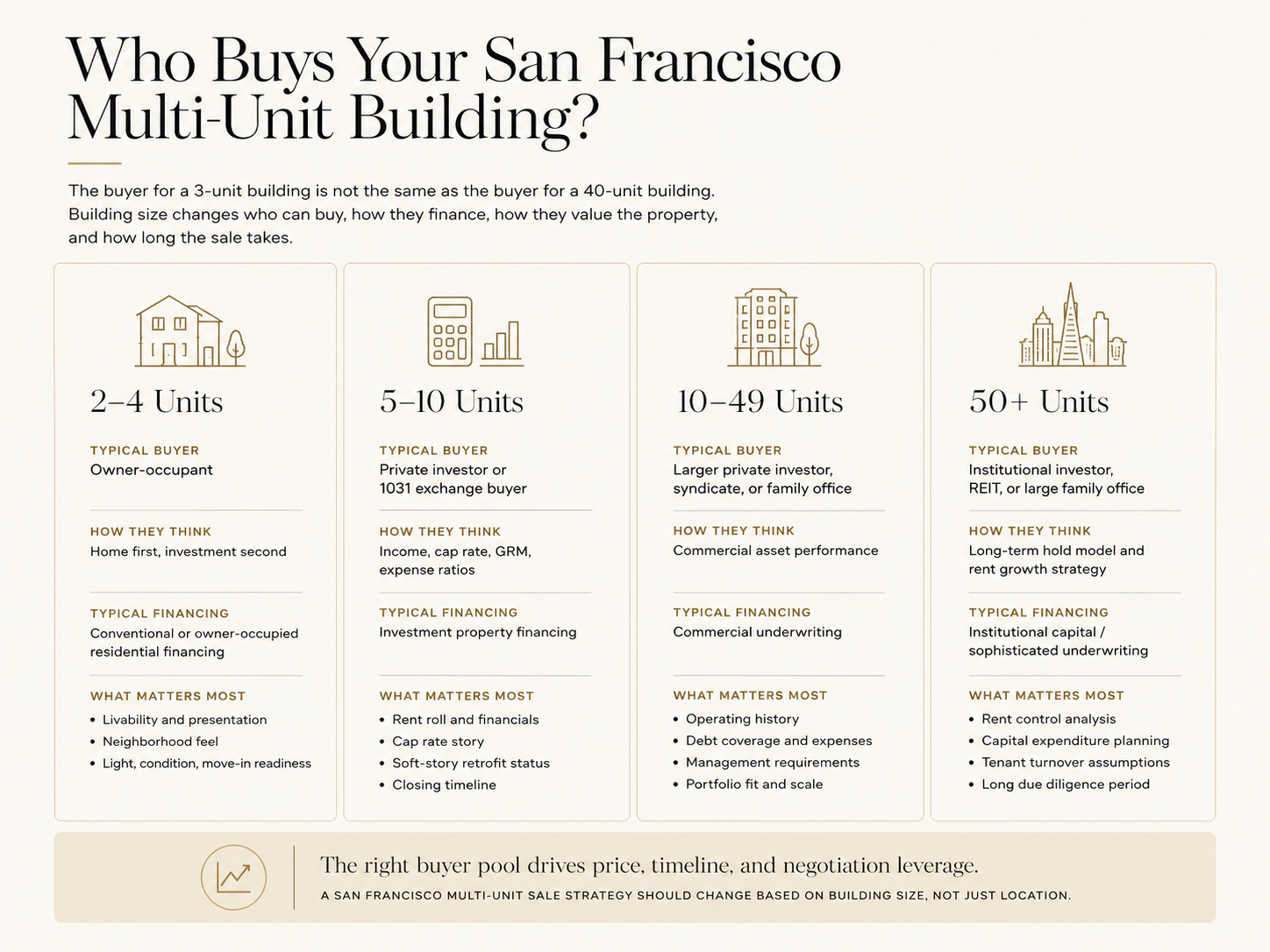

The buyer who shows up for a 3-unit building in San Francisco is not the same buyer who shows up for a 40-unit building. Different people, different financing, different math.

If you own a multi-unit property in San Francisco, this matters more than almost anything else about your sale. The size of your building determines who can even qualify to buy it. That, in turn, shapes your price, your marketing plan, and how long the deal takes to close.

This guide walks through four buyer tiers, starting with small owner-occupied buildings and ending with large institutional portfolios. Each tier pulls from a different pool of capital, and each one has its own rules. Understanding where your building sits helps you price it right and market it to the buyers who can close.

Who Buys 2-4 Unit Buildings in San Francisco

Small multi-unit buildings in San Francisco draw a very specific type of buyer: the owner-occupant. Someone who wants to live in one unit and rent out the others.

These buyers usually finance with conventional loans, and some use FHA-style low down payment programs meant for owner-occupied properties. That financing only works if the buyer plans to live on site, which narrows the pool right from the start.

Owner-occupant buyers rarely think in cap rate. They compare your building to single-family homes nearby, on a per-unit basis. A 3-unit building in the Sunset or Noe Valley often gets valued the way a house would, with rental income treated as a bonus rather than the main event.

This tier is common in neighborhoods like the Richmond District and Noe Valley, where classic Edwardian and Victorian two and three unit buildings line block after block. Buyers here are emotional as well as financial. They're picking a home first and an investment second.

Because emotion plays a bigger role, presentation matters more at this tier than at any other. Clean units, good light, and a move-in ready feel can add real dollars. Allison Chapleau's page on owner-occupied multi-unit properties in San Francisco covers this buyer type in more depth, including how financing timelines tend to run.

Sales at this tier can also move fast once an offer is accepted, since most buyers are represented by residential agents who are used to quick residential-style closings.

The 5 to 10 Unit Apartment Building Buyer Pool in San Francisco

Once a building crosses into the 5 to 10 unit range, the buyer profile changes completely. Owner-occupant financing mostly disappears, and small private investors and 1031 exchange buyers take over.

These buyers think in numbers: cap rate, gross rent multiplier, and expense ratios. A gross rent multiplier compares a building's price to its annual rental income, and it's one of the first filters investors run before digging deeper into the numbers, according to JPMorgan's overview of the metric. Cap rate tells a similar story from a different angle, measuring return relative to price after operating costs.

Many buyers at this tier are also selling something else through a 1031 exchange. This IRS provision lets an investor defer capital gains tax by rolling proceeds from one investment property into another, as long as strict timing rules are met. As explained in Forbes Business Council's rundown of the process, buyers get 45 days to identify a replacement property and 180 days to close. That clock creates real urgency, and it can work in a seller's favor.

Physical building requirements also start to matter here. San Francisco's Mandatory Soft Story Retrofit Program applies to wood-frame buildings with two or more stories over a soft or weak story, five or more residential units, and a construction date before January 1, 1978, according to the city's official Soft Story Retrofit Program page. A building that hasn't completed its retrofit can scare off investors who don't want to inherit that cost or timeline.

335 2nd Avenue, a 10-unit building in the Richmond District, is a good example of how this tier performs when priced and marketed correctly. It drew six offers and sold all-cash for $370,000 over asking, closing in just 15 days to a private investor. That kind of result depends on reaching investors who already understand the numbers, not just buyers browsing listings casually.

Sellers at this tier benefit from clear, well-organized financials. Rent rolls, expense history, and retrofit status should be ready before the property hits the market. Buyers here move fast when the numbers check out, but they walk away just as fast when documentation is messy.

Larger Private Investors and 10 to 49 Unit Building Buyers in San Francisco

Somewhere around 10 units, the buyer pool shifts again. Small private investors give way to larger private buyers, real estate syndicates, and family offices with more capital to deploy.

Financing at this tier moves toward commercial underwriting. Lenders look closely at the building's operating history, the borrower's experience with larger assets, and debt service coverage rather than simple owner-occupant qualification. This slows the process down compared to smaller deals, but it also brings buyers who can handle complexity.

One regulatory detail becomes unavoidable once a building passes 15 units. California requires a resident manager, living on site rent-free, for any apartment building with 16 or more units when the owner doesn't live there, per Stimmel Law's summary of the state's site manager requirements. That's a real staffing and cost line that changes the operating model, and experienced buyers at this tier already factor it into their offers.

Two notable San Francisco sales sit squarely in this tier. 691 Post Street, a 36-unit mixed-use building in Downtown San Francisco, had an accepted offer in just two weeks. It traded at a 4.32% cap rate and a 12.73 gross rent multiplier, and it sold to private investors who understood exactly what those numbers meant for their return.

625 Scott Street, a 42-unit building across from Alamo Square, sold for $18,050,000 in 2022, the largest and most expensive multifamily sale in San Francisco that year. It drew four offers and closed non-contingent. The Real Deal, a commercial real estate trade publication, reported the winning buyer was a local investor with other Bay Area holdings, the kind of experienced, well-capitalized buyer this tier attracts.

Buildings in this range also show up in neighborhoods like NOPA, the Mission, and Eureka Valley, where larger apartment stock sits alongside smaller Victorians. 250 Douglass Street, a 16-unit historic building in Eureka Valley, sold for $5,850,000 with a full-price offer in 21 days, to a private investor expanding their neighborhood portfolio. That's a familiar pattern at this tier: buyers who already own nearby and want to add scale.

Marketing a building this size means reaching people who track San Francisco's multi-unit market closely, not casual home shoppers. Allison Chapleau's notable multi-unit sales in San Francisco page shows the kind of track record that gets serious buyers to pay attention early.

Institutional Buyers for Large Apartment Buildings in San Francisco

Above roughly 50 units, the buyer pool narrows to a small group of well-funded players: institutional investors, real estate investment trusts, and larger family offices with dedicated acquisition teams.

These buyers underwrite differently. They run detailed models on rent growth, capital expenditure needs, tenant turnover, and long-term hold strategy before making an offer. Expect a longer due diligence period than at any smaller tier, often stretching several months instead of weeks.

Because the buyer pool is small, marketing has to reach a completely different network of capital. That means direct outreach to acquisition teams, institutional brokers, and investment groups that specialize in large multifamily assets, rather than a standard listing campaign aimed at the general public.

San Francisco's rent control ordinance adds another layer at this tier. Buildings with long-term tenants under rent control require careful valuation, since in-place rents can sit well below market. Institutional buyers model this carefully, and sellers need an agent who understands how to present that data clearly.

Pricing accuracy matters enormously here, since even small percentage errors translate into large dollar swings on a building this size. A seller who misjudges the market at this level can lose serious money, or scare off the exact buyers who could close the deal.

How Building Size Changes Price, Marketing, and Timeline in San Francisco

Every tier shift changes three things: who can buy, how the building gets valued, and how long the sale takes.

Smaller buildings sell to emotional, owner-occupant buyers using residential-style financing, and they often close quickly once a price is agreed. Mid-size buildings sell to investors who need solid financials and clean retrofit records before they'll move. Large buildings sell to a small, sophisticated pool that needs months of underwriting before committing.

Pricing strategy has to match the tier too. A 3-unit building in Noe Valley gets compared to houses nearby. A 40-unit building near Alamo Square gets compared to cap rates on similar assets across the city, not to homes on the same block.

Sellers who understand this ahead of time avoid a common mistake: marketing a mid-size or large building the same way they would a duplex. Reaching the right buyer pool, a 1031 exchange buyer, a family office, or an institutional acquisition team, is what drives price and speed.

Working with an agent who has closed deals across every tier, from small Richmond District buildings to 40-plus unit properties downtown, gives sellers a real advantage. That range of experience is part of what makes Allison Chapleau the top multi-unit realtor in San Francisco for owners trying to figure out where their building fits and who's likely to buy it.

Sellers dealing with an inherited property, a trust, or a partition sale face an added layer of complexity on top of all this. Allison's page on probate and trust sales in San Francisco walks through how court-confirmed sales work alongside these buyer pool dynamics.

Before listing, it helps to see where current market data on cap rates, days on market, and price per unit stand across San Francisco. The San Francisco market reports page and the San Francisco market insights page both track this by neighborhood and building size, and they're a useful starting point before setting a price.

Owners who want a specific number for their own building can request a property valuation for their San Francisco multi-unit building directly. Buyers on the other side of the transaction can review sold multi-unit properties in San Francisco to see how recent deals closed at each tier.

Frequently Asked Questions About Buyer Types for San Francisco Multi-Unit Buildings

Who typically buys a 2-4 unit building in San Francisco?Owner-occupants make up most of the buyer pool for small multi-unit buildings in San Francisco. They often use conventional or FHA-style loans and plan to live in one unit while renting the others in neighborhoods like the Sunset or Noe Valley.

Do 5 to 10 unit buildings in San Francisco sell to different buyers than smaller properties?Yes. Buildings in this range in San Francisco mostly attract small private investors and 1031 exchange buyers who evaluate cap rate and gross rent multiplier rather than comparing the building to a house.

What is the soft story retrofit rule for multi-unit buildings in San Francisco?San Francisco's Mandatory Soft Story Retrofit Program applies to wood-frame buildings built before 1978 with five or more units and a soft or weak story condition. It's a real cost factor that investors in San Francisco weigh heavily once a building reaches five units.

When does a resident manager become required for an apartment building in San Francisco?California law requires a resident manager living on site once a building reaches 16 or more units and the owner doesn't live there. This threshold shapes how larger private investors and syndicates underwrite buildings in San Francisco in the 10 to 49 unit range.

How does financing change for larger multi-unit buildings in San Francisco?Smaller buildings in San Francisco often qualify for residential-style loans, but buildings above roughly 10 units shift toward commercial underwriting. Lenders evaluate the building's income history and the buyer's experience rather than simple owner-occupancy.

Who buys 50-plus unit apartment buildings in San Francisco?At this size in San Francisco, the realistic buyer pool is institutional investors, REITs, and larger family offices with dedicated acquisition teams. These buyers take longer to underwrite a deal, often several months, before making a decision.

Does rent control affect how multi-unit buildings are valued in San Francisco?Rent control changes valuation quite a bit for buildings with long-term tenants in San Francisco. In-place rents can sit below market, and buyers at every tier factor this into their offers, especially on larger properties.

How long does it take to sell a multi-unit building in San Francisco?Timelines vary by tier in San Francisco. Small owner-occupant sales can close in a matter of weeks, mid-size investor deals often move in under a month when the numbers are solid, and large institutional sales can take several months of underwriting.

What is a 1031 exchange and how does it affect multi-unit buyers in San Francisco?A 1031 exchange lets an investor defer capital gains tax by reinvesting sale proceeds into another investment property. Buyers using this strategy in San Francisco face strict deadlines, typically 45 days to identify a new property and 180 days to close.

Why does building size matter so much when pricing a multi-unit property in San Francisco?Building size in San Francisco determines who can buy, how they finance the purchase, and what valuation method they use, a per-unit comparison or a cap rate model. Getting the tier right is central to setting an accurate price and reaching buyers who can close.

If you own a multi-unit building anywhere in San Francisco, from a small duplex in the Richmond District to a large property near Downtown or Alamo Square, Allison Chapleau can walk you through exactly who's likely to buy it and what that means for your price. Reach out to Allison Chapleau to talk through your San Francisco building's next sale.